If there is one thing certain, it is that the “hunt” for carbon is just beginning and will intensify in the years to come. In France, where the government has presented its ecological planning to achieve the target of 55% reduction in CO2 emissions by 2030, in Europe, where the European Commission is implementing the Green Deal or across the world with American or Chinese competition.

Exceptional climate events are multiplying, the carbon constraint is increasing and consumers are taking responsibility. In short, the fight against climate change is disrupting the activity and strategy of companies.

How to successfully move away from carbon? How to successfully transition to another business model? How to protect yourself from climate risks?

For companies, one tool appears more essential than ever: that is the GHG inventory. It allows the company to measure its dependence on carbon and thus measure the risks of an unexpected transition. It is also the crucial starting point of any strategy to reduce greenhouse gas (GHG) emissions. Mitigation and adaptation: these are the two major challenges in the coming years and in both cases, the GHG inventory forms an integral part.

1. What is a carbon footprint?

A carbon footprint is a snapshot at a given moment of all the GHG emissions of a company.

But what we call the carbon footprint is in reality the name of a method used to calculate the carbon footprint. Method developed by the government and the ADEME, finally launched in 2004. Its name: the Carbon Footprint®. The methodology is rapidly deployed and becomes the reference tool. So much so that its name has passed into common language and the measurement of the carbon footprint of a company, a community, an association or even a sporting competition is commonly called a carbon footprint. The methodology, meanwhile, is now managed by the Association for the Low-Carbon Transition (ABC).

The Carbon Footprint® is not the only existing methodology for measuring the carbon footprint. In France, there is also the mandatory greenhouse gas (GHG) assessment. This device provides for the mandatory implementation of an emissions assessment and an action plan to reduce them for companies with more than 500 employees and communities with more than 50,000 inhabitants.

Two other international methodologies exist: the GHG Protocol and the ISO 14069 standard. The Sami platform and our consultants are able to manage these different methodologies and to switch from one to the other according to the needs and demands of companies.

Difference between carbon footprint and Carbon Footprint®

2. Why do a carbon footprint?

2.1 Regulation

Regulation is gradually tightening on the measurement of companies' carbon footprint and the reduction of their GHG emissions.

French regulation

Article L. 229-25 of the Environmental Code, provides for the implementation of a mandatory greenhouse gas (GHG) assessment for:

- les personnes morales de droit privé employant plus de 500 salariés en France métropolitaine

- legal entities of private law employing more than 250 employees in the overseas regions and departments

- communities of more than 50,000 inhabitants and other legal entities of public law (hospitals, etc…) employing more than 250 people

The mandatory greenhouse gas inventory must be renewed every 4 years for companies and every 3 years for local authorities and public law entities.

On April 2, 2025, the National Assembly adopted the draft law known as the adaptation to the law of the European Union. Companies subject to the CSRD and which publish their greenhouse gas emissions report as well as a transition plan within this framework will now be exempt from the obligation to establish and publish a BEGES.

Read our complete article dedicated to the BEGES.

European regulation

The CSRD

La directive européenne sur la CSRD intègre les enjeux climatiques dans le reporting extra-financier de toutes les entreprises de plus de 1000 collaborateurs. The complete carbon footprint is indeed among the information expected in this reporting.

On this subject, you can consult our article dedicated to the ESRS E1 on climate change.

Ce mardi 9 décembre 2025, après des mois de discussions, les négociateurs des pays membres de l’Union européenne et du Parlement européen sont parvenus à un accord final sur la directive Omnibus simplifiant la CSRD.

Voici les principaux changements actés :

- Relèvement significatif des seuils : 1 000 salariés (contre 250 auparavant) et 450 M€ de chiffre d'affaires

- Exclusion définitive des PME cotées et des holdings financières

- Introduction d'une clause de réexamen pour un éventuel élargissement futur du périmètre

Cet accord a été adopté définitivement par le Parlement européen, réuni en plénière, le mardi 16 décembre.

Le texte doit être maintenant formellement approuvé par le Conseil. La directive entrera en vigueur 25 jours après sa publication au Journal officiel.

Read our article dedicated to the Omnibus directive and the envisaged changes on the CSRD, CSDDD, and European Taxonomy.

La VSME pour les entreprises qui sortent du cadre CSRD

The VSME standard (Voluntary standards for non-listed Small and Medium-sized Enterprises) is a reporting framework published by the EFRAG in December 2024 and initially designed for VSEs and SMEs not subject to the CSRD.

En février 2025, la Commission européenne annonce vouloir créer un nouveau cadre de reporting volontaire pour toutes les entreprises qui ne seront plus soumises à la CSRD. And European legislators say they want to draw heavily on the VSME to build this new voluntary framework. The VSME standard will therefore be used by thousands of European companies in the coming months and years and thus take on strategic importance.

It will enable:

- To guide companies in identifying and managing their sustainability issues

- To enable companies to publish a sustainability report following a standardized methodological framework

- To improve transparency on companies' ESG commitments

- To facilitate the transmission of information to partners subject to the CSRD

In its complete module, the VSME recommends conducting a carbon footprint covering scopes 1 and 2, as well as significant emissions from scope 3.

Read our complete article on the VSME standard

Access our VSME indicators checklist

2.2 A strong competitive challenge

Risks to economic performance

"Doing a carbon footprint is a first step to managing and addressing the climate risks to which a company is exposed"

Guillaume Colin, Head of Climate Expertise at Sami.

- Risks related to stakeholders

An increasing number of companies are asking their suppliers to produce at least the carbon footprint of their activity. Let's mention SNCF, which has been integrating since 2023 for its 55 largest suppliers a carbon ton price in its tenders in order to monetize their GHG emissions.

- Financing risks

The investment funds and banking partners are increasingly numerous to require companies in their portfolio or their clients at least the calculation of their carbon footprint, for others the implementation of a decarbonization strategy.

- Market risks

"Carbon prices are rising. If a company wants to know its exposure to this carbon financial risk, the starting point is to know its emissions. If it does not know to what extent its value chain is carbon-intensive, it risks paying much more for its raw materials or being less competitive downstream because these carbon taxes will erode margins."

Guillaume Colin

- Physical risks

Heatwaves, floods, droughts: the impacts of climate change can affect the entire value chain of the company.

The opportunities

For the same reasons that not engaging in a transition approach exposes the company to many risks, doing so offers prospects for economic benefits: competitive advantage, access to financing, etc... This also allows you to benefit from CSR labels or certifications, such as Ecovadis or B-Corp.

Read our article on the economic benefits of conducting a carbon footprint.

2.3 Employer Brand and Legal Risk

According to this study published by the Unedic in April 2023, 84% of French workers want a job in line with the climate challenge and ¼ of workers are considering changing jobs or companies to align their professional life with their ecological concerns.

The risk is also legal. Lawsuits against companies accused of not implementing a realistic emissions reduction strategy are multiplying. According to a study by the Grantham Institute of the London School of Economics, published in 2023, the filing of a complaint results in an average reduction of 0.57% in the value of the targeted company. And an unfavorable judgment an average decrease of 1.5% in the stock price.

To delve deeper into the subject of climate risks that weigh on companies, to know how to identify them and how to adapt, you will find here a complete article.

2.4 An Ethical Issue

At the current rate, 1.5°C will be exceeded during the next decade, 2°C around 2050 to reach 3 or 4°C in 2100, causing devastating, widespread, sometimes irreversible impacts.

But this worst-case scenario is still avoidable. Solutions exist and companies have a key role to play.

You will find here the article on the reasons why the carbon footprint is an essential tool in a company's strategy.

{{newsletter-blog-3}}

3. The main steps of a carbon footprint

3.1 Define the scope of the study

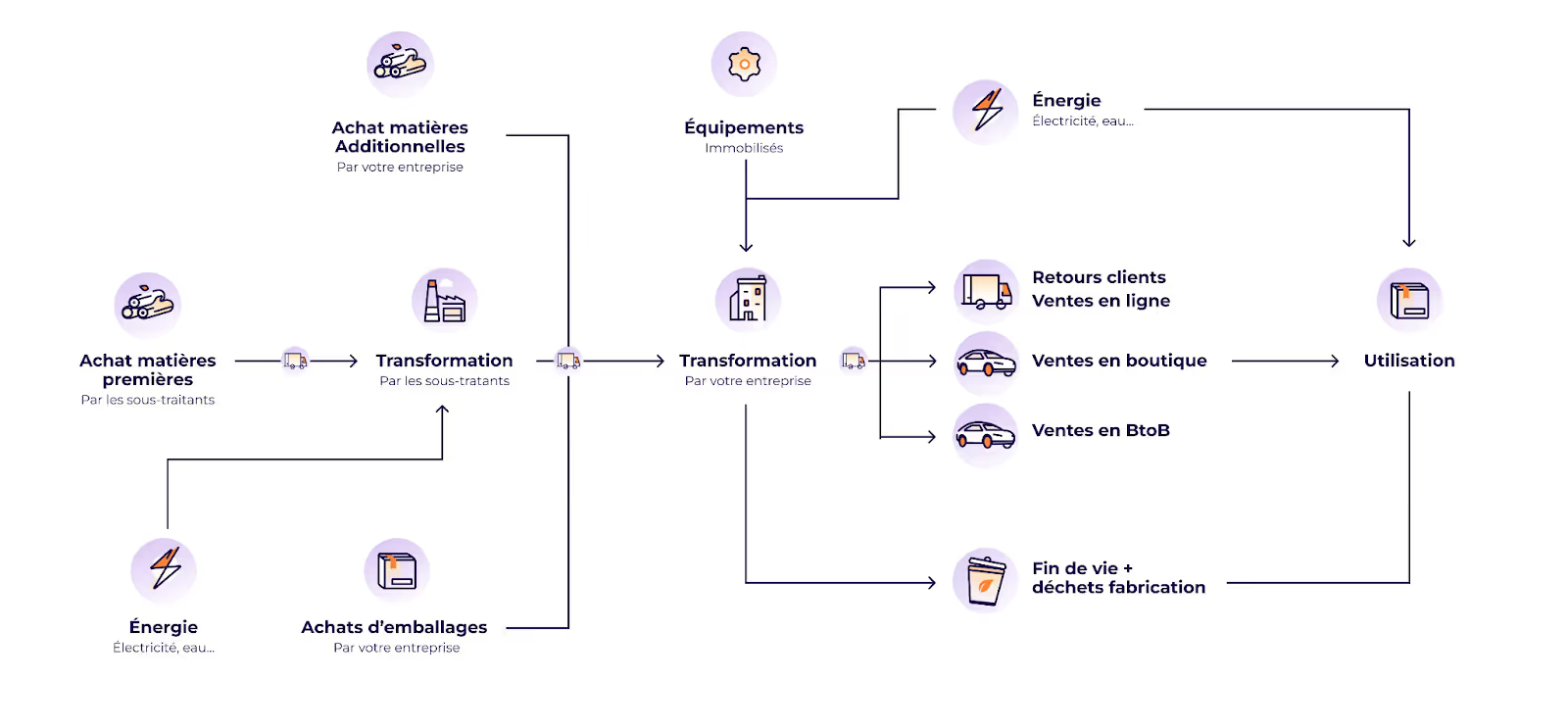

The first step is to map the flows of energy, raw materials, waste, and products generated by the company.

This step is essential to properly determine what will be taken into account in the carbon footprint calculation.

3.2 Data collection

The calculation of the carbon footprint is based on the activity data of the organization. These must therefore be inventoried and then collected. They are then transformed into quantities of CO2 equivalent thanks to emission factors, we will come back to this.

Collection is therefore one of the most important moments. The more precise and exhaustive the data retrieved, the more important the accuracy of the carbon footprint will be. It is therefore essential to work on an effective and relevant collection, all the more so as this step is the most time-consuming phase of the process.

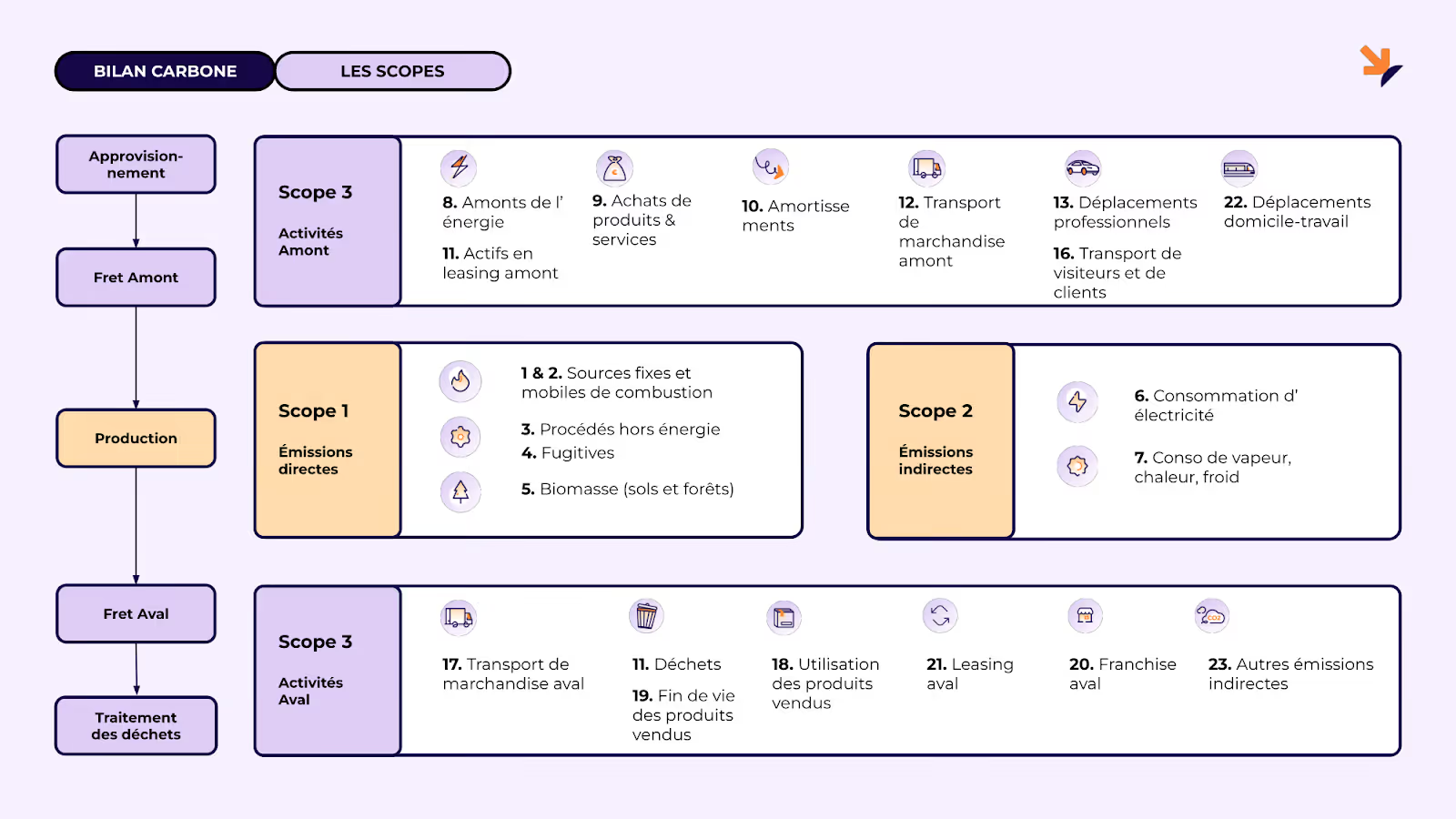

These data must reflect, as we have said, all the direct and indirect emissions of the company. This is where the famous scopes 1, 2, and 3 come into play since the two main methodologies, Bilan Carbone® and GHG Protocol, categorize emissions into these 3 distinct scopes.

- Scope 1: these are the company's direct emissions.

Example: the gas heating of the company's offices or the fuel used for the company's vehicles.

- Scope 2: these are indirect emissions related to energy.

Example: electricity consumption.

- Scope 3: these are all other indirect emissions of the company. Scope 3 generally represents the vast majority of the company's activity emissions, sometimes up to 95%.

Example: the purchase of services or raw materials, business travel, home-to-work travel, freight, or the use of products.

The Bilan Carbone® thus lists 23 different emission items, which you can find in the graph above. These are the data associated with these different items that the company must collect.

3.3 Consolidation

Once the collection is complete, the next step is the consolidation of the data. This is a key phase as it ensures, for the consultants who accompany the company in measuring its carbon footprint or for the company that carries it out internally, that the data collected is indeed the correct data, that there are no inconsistencies, obvious errors, omissions and duplicates in the measurement of emissions.

Example of a possible duplicate: in the case of company electric vehicles, the emissions related to electricity consumption will be counted in travel (through the kilometers traveled for example) while these vehicles are often recharged in the company's premises. The electricity consumed is then also accounted for in the general consumption of the premises. It must therefore be removed to avoid a duplicate.

3.4 Analysis of results

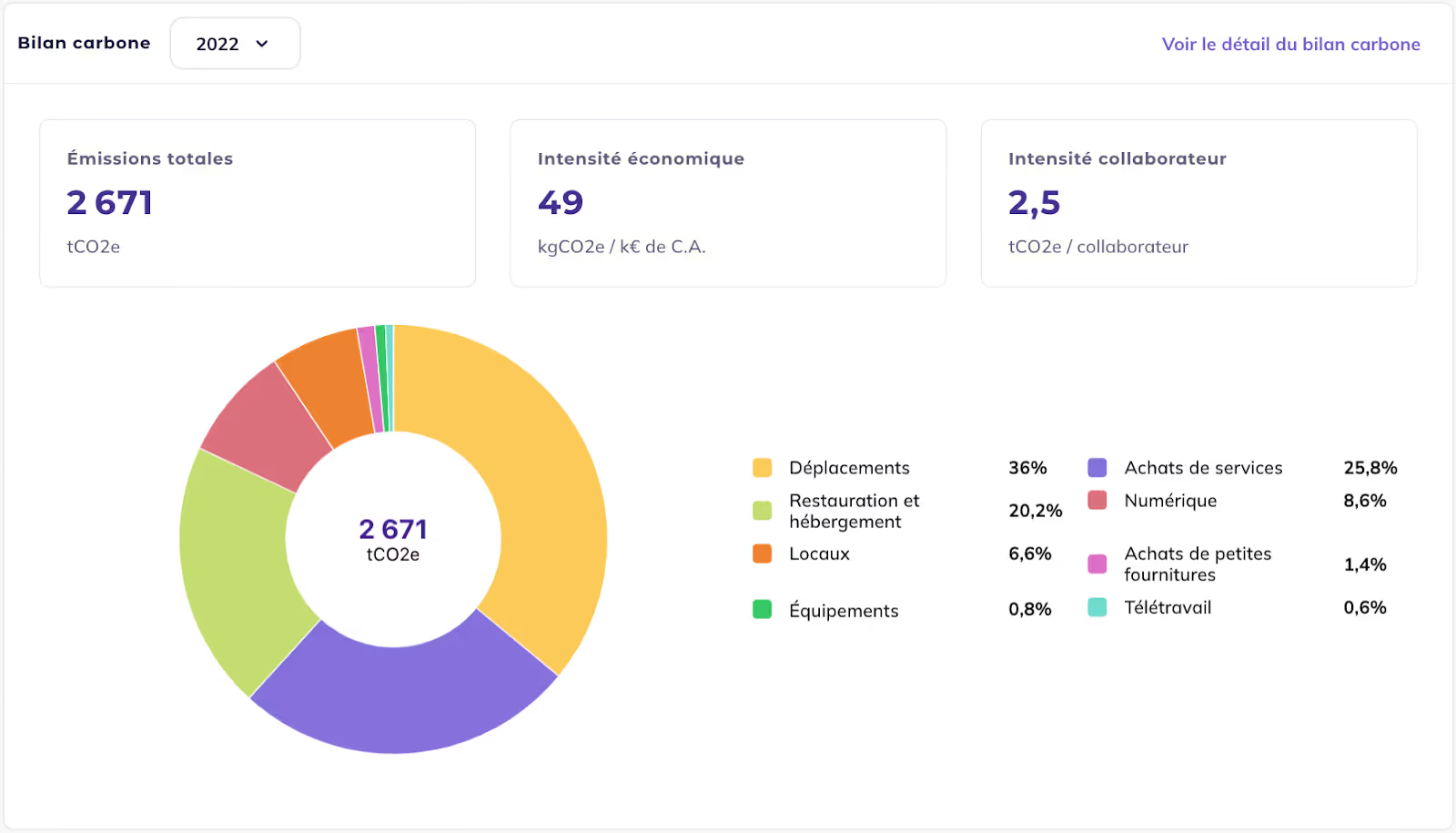

Two different but complementary approaches allow to read and analyze the results of the carbon footprint.

- The first is a general approach. The results of the carbon footprint are presented with the total of GHG emissions. These emissions are distributed by scope (1, 2 and 3) and by categories. This approach allows to have a first vision of the distribution of these same emissions according to their categories. For example, are the emissions from travel or premises the most significant?

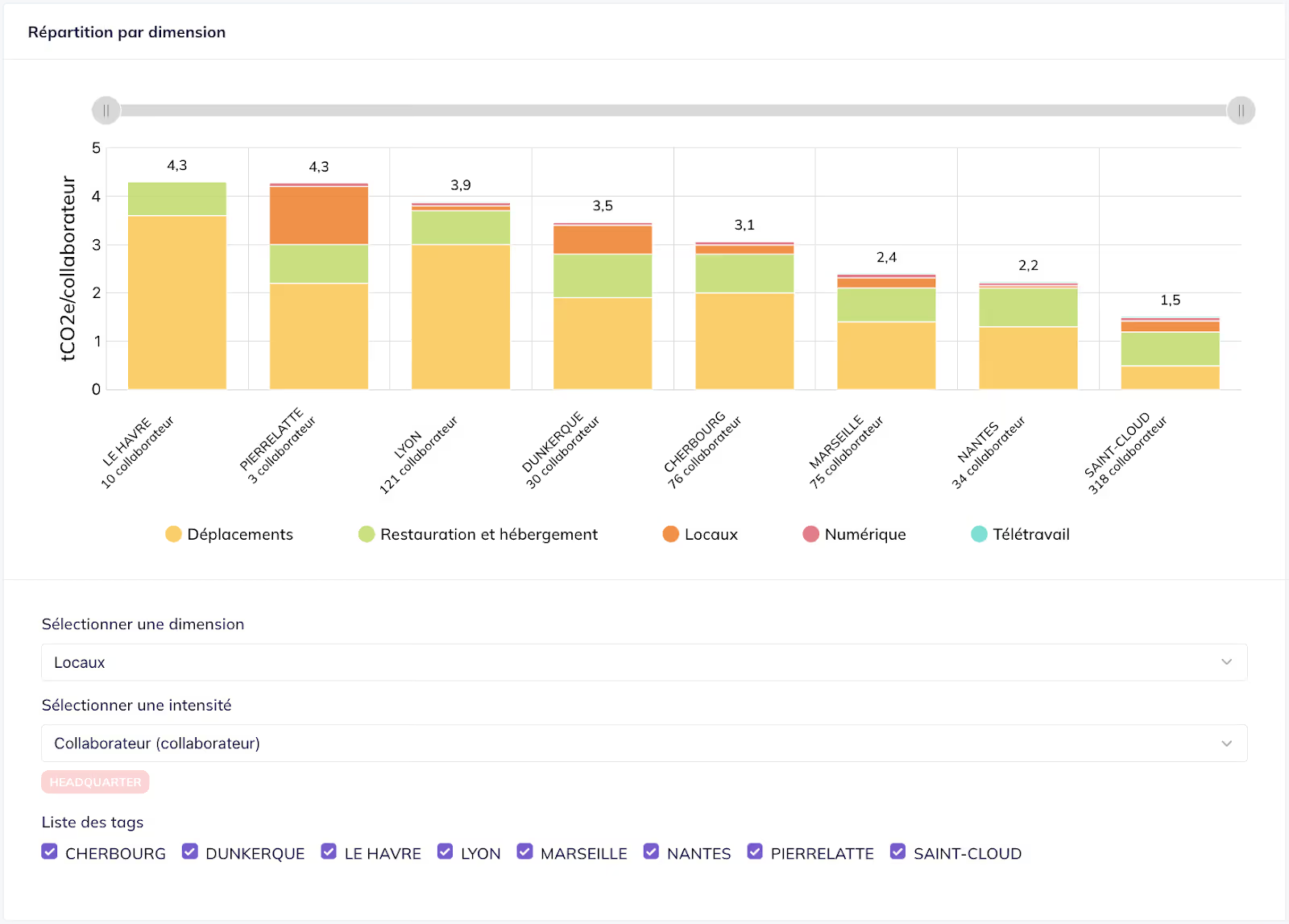

- However, this general approach only partially allows to effectively analyze the sources of greenhouse gas emissions. This is where the analytical approach comes into play. It allows to distribute the emissions according to their categories obviously but also according to the activities of the company and therefore to detail them much more finely. The company is then able to identify its carbon dependence for example by product, by subsidiary, by supplier, by country or even by office or factory if it has several.

For example, here, on this anonymized carbon footprint, an analytical approach with a carbon intensity per employee and per site of the company.

3.5 Action plan

Measuring greenhouse gas emissions is not an end in itself. It is the starting point of a strategy to reduce emissions. Because you only reduce what you know.

And this strategy must materialize through an action plan.

The action plan is an integral part of the carbon footprint. It is mandatory in the realization of a Bilan Carbone® and is part of the support device within the framework for example of the Diag Decarbon'Action device.

{{newsletter-blog-3}}

4. How to measure emissions?

We are now entering the heart of carbon footprint measurement. Once the activity data of the company, the community or the association has been collected, it must be transformed into CO2 equivalent (CO2e).

To do this, you need to associate the activity data with an emission factor.

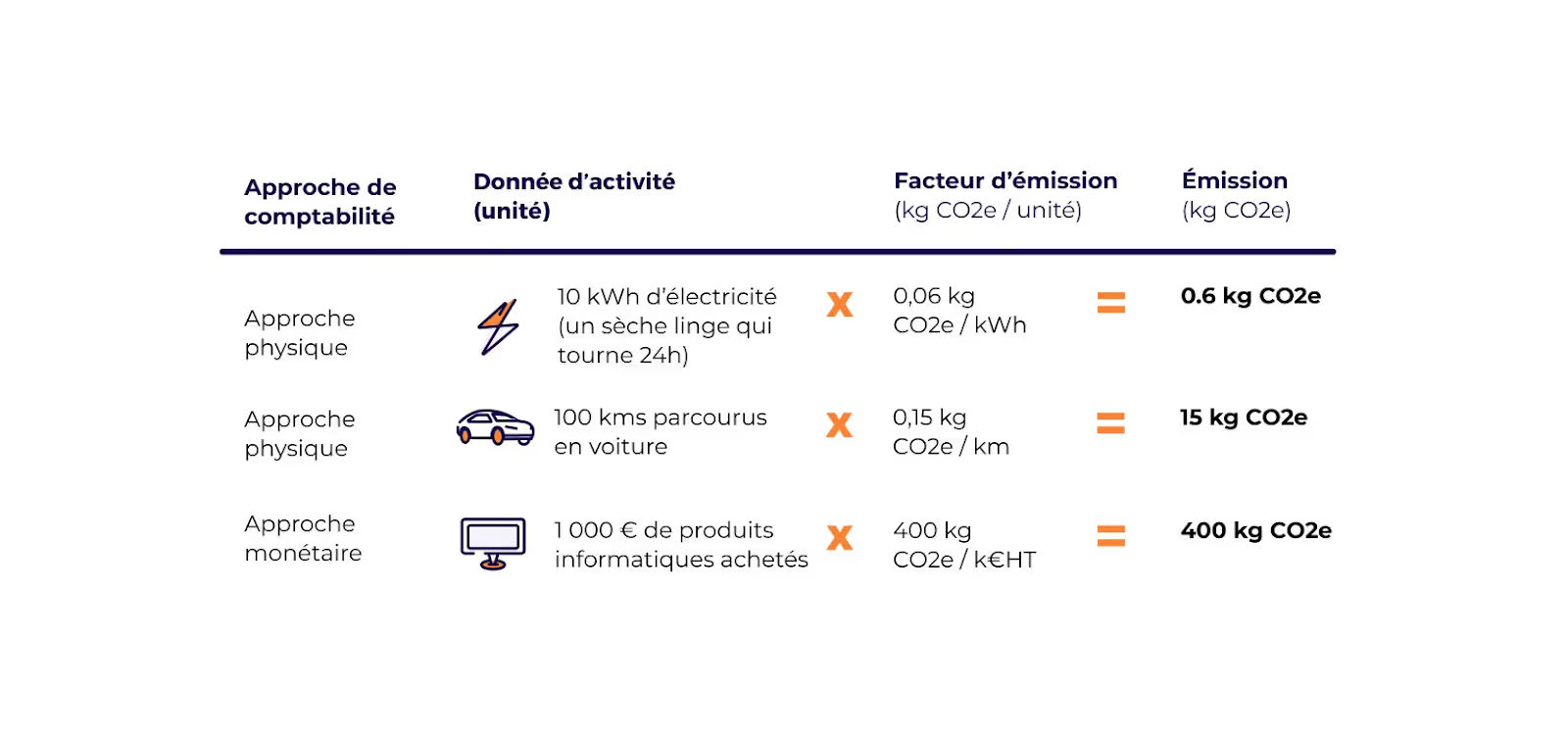

4.1 Monetary or physical approach?

Two types of data can be used and this then changes the way the associated emissions are calculated:

- Financial data: we are talking about a bill or a monetary amount. In this case, the monetary amount is converted into CO2e emissions. We are talking here about a monetary approach.

- Physical data: this can be distances traveled (km), quantities used (kWh, kg, tonnes, etc.). These physical data are converted into CO2e emissions. We are talking here about a physical approach.

Which approach is used? Both are complementary even if the physical approach remains indispensable to gain in precision and to match the reality of the company's activities.

The monetary approach notably allows to quickly and simply calculate the emissions linked to service expenses mainly. We think of the purchase of intellectual services or studies, marketing or communication expenses, banking services, fees, etc. All these expenses are quite unsuitable for a physical approach whereas they are quite simple to integrate into the carbon footprint thanks to a monetary approach. Indeed, it is possible to collect and add these expenses automatically thanks to the FEC, the General Accounting Journal. The monetary approach is also suitable for the financial sector, for example to assess the associated emissions of an investment portfolio.

However, the monetary approach is not suitable for all other emissions. This is particularly the case for emissions throughout the life cycle of a product: raw materials, manufacturing, packaging, freight, use, etc. The company's energy consumption, home-to-work travel or business travel should also be considered under a physical approach. It is essential in these cases in order to obtain precise emissions that reflect the physical reality of the company's activities.

Example: for home-to-work travel, using a monetary ratio with fuel expenses would significantly vary the associated emissions due to the very large variation in the price per litre of petrol, even though the actual emissions would have remained the same. The same applies to energy consumption with the volatility of energy prices. The physical approach is therefore often unavoidable. And because it allows a better identification of the organisation's real emissions, it allows a better evaluation of its carbon dependence and therefore subsequently to build a more relevant and effective low-carbon strategy.

4.2 Emission factors (EF)

This is the indispensable tool for calculating the carbon footprint, the gear that allows you to move from the collected activity data to the associated emissions.

Each activity data is thus converted thanks to the emission factors, monetary emission factor (or monetary ratio) when the activity data is expressed in monetary amount or physical emission factor when the data is expressed in physical activity (distance, quantity, etc.).

These EFs, physical and monetary, are found in different databases, public and private. Each of these databases has different characteristics, with different information.

Finding the right emission factor to associate with each activity data is often time-consuming. This is why, to simplify the work of consultants or companies while increasing the accuracy of carbon footprints, Sami has been developing a consolidated emission factor database for years.

It now contains more than 230,000 emission factors, from more than 25 reference source databases.

To find out more about this consolidated EF database, how it was built and how it is updated, you can go to the article dedicated to emission factors.

5. Choosing the right software solution for your carbon footprint

Defining the scope of your project

Before selecting a software, ask yourself the following questions:

- What is the structure of your company?

- What scope do you want to measure (group, subsidiaries, specific activities)?

- Do you need a consolidated and/or detailed view?

Key features to evaluate

- Collaboration with consulting firms

- Possibility to work with your current firm

- Network of experts in your sector

- Adaptation to your organisation

- Management of organisational units (subsidiaries, BU, countries, sites)

- Customisation according to your structure

- Management of rights and access

- Setting up access according to user roles

- Protection of sensitive data

- Quality of emission factors

- Databases used (Base Carbone®, sectoral...)

- Regular updates

- Possibility to add custom factors

- Data collection systems

- Customisable collectors and questionnaires

- Import of CSV/Excel files

- API available

- Analysis of results

- Visualisation by organisational unit

- Customisation of categories

- Calculation of carbon intensities

- Draft of an action plan

- Modeling the impact of actions

- Catalog of decarbonization actions

- Custom actions

- Reduction trajectory

- Definition of absolute and intensity objectives

- Alignment with SBTi methodologies

- Taking into account economic growth

- Regulatory reporting

- Export to BEGES, GHG Protocol formats

- Compliance with CSRD/ESRS/VSME

{{newsletter-blog-2}}

6. Training to conduct a Carbon Footprint®

Our training organization, Sami Academy, is a partner of the ABC, the Association for the Low Carbon Transition, and is authorized to train in the Carbon Footprint® method.

Two training paths are available:

- Carbon Footprint® - Introduction

This training enables you to master the fundamentals and to carry out an internal Carbon Footprint® recognized by the ABC.

It is intended for:

- for companies, local authorities and other organizations wishing to carry out their Carbon Footprint® internally

- For consultants who wish to become Carbon Footprint® providers and sell Carbon Footprint® implementation services by combining this training with the Carbon Footprint® - Mastery training

Details of the Carbon Footprint® - Introduction training

- Carbon Footprint® - Mastery

This training enables you to achieve an advanced level of mastery of the Carbon Footprint® methodology and to become a Carbon Footprint® provider certified by the ABC.

The training is intended for:

- for all those wishing to have an advanced level of the Carbon Footprint® method (CSR managers, carbon managers…)

- for consultants who wish to sell Carbon Footprint® services

Details of the Carbon Footprint® - Mastery training

Read our article to choose your carbon footprint training

7. How to finance your carbon footprint?

Diag Decarbon'Action

Diag Decarbon'Action is a device to support companies in carrying out a carbon footprint. This offer is operated by Bpifrance, co-financed by the ADEME.

The Diag includes the realization of a carbon footprint, the co-construction of a climate strategy to reduce greenhouse gas emissions and support in the implementation of the first measures of the action plan.

Eligible are companies with fewer than 500 employees that have never carried out a carbon footprint before. After subsidy, the price is 6000 euros.

Read our article dedicated to Diag Decarbon'Action

8. Testimonials: these companies that have carried out their carbon footprint with Sami

- Intersport

"Sami brings all this finesse in the analysis and management of our carbon data"

Read the testimonial of Claire Gautier-Le Boulch, CSR Manager of Intersport

- West France

"Sami helped us move from a regulatory carbon footprint to an actionable carbon footprint"

- La Rosée

"We are convinced that this is what will guarantee our robustness in 10 or 20 years"

Read the testimony of Laure-Anne Dumas, CSR Director of La Rosée

- Leroux and Lotz Technologies

"We are committed to putting climate impact at the heart of the company's strategy"

Read the testimony of Amélie Di Bona, CSR Mission Manager Leroux and Lotz Technologies

Discover all our clients' testimonials

{{newsletter-blog-3}}

FAQ: Frequent questions about the carbon footprint

What is the cost of a carbon footprint?

The cost varies considerably depending on the size of the company and the complexity of its activities. For an SME, it can range from a few thousand euros (digital solution in autonomy) to several tens of thousands of euros (complete support by a specialized firm).

How long does it take to carry out a carbon footprint?

On average, count 2 to 6 months for a first complete carbon footprint, including data collection, analysis, and the development of the action plan. Subsequent iterations are usually faster.

Can carbon footprints be compared between companies?

Direct comparison is difficult due to methodological differences, scope, or sector of activity. It is preferable to focus on the evolution of its own emissions over time or to use specific sector benchmarks.

What is the difference between carbon compensation and reduction?

Reduction consists of actually decreasing emissions at the source. Compensation consists of funding projects that sequester or avoid emissions elsewhere. Priority must always be given to reduction.

Is the carbon footprint mandatory for all companies?

No, obligations depend on the size and status of the company. Following recent changes to the CSRD, detailed reporting obligations mainly concern companies with more than 1000 employees. For SMEs, the BEGES-r applies from 500 employees, and voluntary reporting (VSME) is recommended for others.

Articles that might interest you on the same subject

The best carbon footprint software in 2025: how to choose the ideal solution for your company

What is the definition of emission Scopes 1 2 3?`

Calculating Scope 3 in a carbon footprint: what are the different approaches?

Carbon footprint training: which one to choose in 2025?

The best financing options to structure, strengthen, and accelerate your low-carbon transition

Mission Décarbonation

Don't miss the latest climate news and stay ahead of regulatory changes

How to build your RFP for a carbon software?

Discover our guide that will guide you step by step to select the best software according to your needs. Discover an exclusive ready-to-use Excel document to build your RFP!

Your carbon footprint with Sami

Sami accompanies you in measuring your emissions and building your action plan

Les commentaires