Double materiality has become a central concept in the sustainability reporting of European companies. This fundamental principle, which combines the analysis of financial and extra-financial impacts, constitutes the cornerstone of the CSRD (Corporate Sustainability Reporting Directive) which came into force on January 1, 2024.

Faced with climate and societal challenges, companies must now respond to the growing expectations of transparency from their stakeholders. Employees, consumers, and investors demand a clear and comprehensive view of the global impact of activities on society and the environment.

Double materiality precisely addresses this issue by offering a comprehensive methodological framework to assess the sustainable performance of companies from two complementary angles:

- Financial materiality ("Outside-In" vision): how the economic, social, and natural environment affects the company's financial performance

- Impact materiality ("Inside-Out" vision): how the company impacts its economic, social, and natural environment

This concept, defended by the EFRAG (European Financial Reporting Advisory Group) and integrated into the ESRS (European Sustainability Reporting Standards), differs significantly from the Anglo-Saxon approach of the ISSB, which focuses solely on simple materiality. The EFRAG and the ISSB nevertheless published in May 2024 a guide on the interoperability between these two sets of standards in order to facilitate compliance by companies.

The European Commission has chosen to make the themes covered by the CSRD reporting conditional on this double materiality analysis, making this methodology an indispensable prerequisite for companies subject to the directive.

Carrying out a double materiality analysis represents a strategic tool for organizations. In this article, we explain in detail what double materiality is, why it is essential to your sustainability strategy, and above all how to implement it effectively to meet the requirements of the CSRD.

1. What does the concept of double materiality cover?

Double materiality is a tool for building the CSR strategy of companies. It is a comprehensive process consisting of identifying and prioritizing the most important environmental, social, and governance (ESG) issues for a company and its stakeholders.

The concept of double materiality corresponds to the analysis of two types of materiality: financial materiality and impact materiality (or extra-financial).

- Financial materiality or simple materiality corresponds to the "Outside-In" vision: it only takes into account the positive (opportunities) and negative (risks) impacts generated by the economic, social, and natural environment on the development, performance, and results of the company. This first dimension therefore concerns financial aspects: revenues, profits, cash flows, etc.

- Impact materiality or extra-financial socio-environmental materiality corresponds to the "Inside-Out" vision. It takes into account the negative or positive impacts of the company on its economic, social, and natural environment and therefore encompasses environmental, social, and governance (ESG) impacts.

With this concept of double materiality, companies must therefore report both the impact of society and the environment on their financial performance and the impact of their activities on society and the environment.

2. Double materiality in 2025

2.1 For companies with more than 1000 employees

On February 26, 2025, the European Commission presented its legislative proposals (Omnibus) to simplify sustainability texts, notably the CSRD.

Here are its main proposals:

・Reduce the scope: reporting requirements would only apply to large companies with more than 1,000 employees (and either a turnover of more than 50 million euros, or a total balance sheet of more than 25 million euros). The number of companies concerned would be reduced by approximately 80%.

・For companies that are no longer concerned, the Commission will adopt a voluntary reporting standard by delegated act, based on the VSME standard.

・Only this information can be requested by companies subject to the CSRD and wishing to obtain information from their value chain companies with fewer than 1,000 employees.

・The Commission would like to revise the European sustainability reporting standards (ESRS) in order, among other things, to substantially reduce the number of data points.

・Postpone by two years the entry into force of the reporting requirements for large companies that have not yet started to implement the CSRD and for listed SMEs (waves 2 and 3) to avoid them starting their report when they may be excluded from the scope if the Commission's proposals are confirmed.

On the other hand, the European Commission clearly indicates that the principle of double materiality is not called into question. All companies within the scope of the CSRD will therefore have to carry out a double materiality analysis in accordance with the ESRS.

2.2 For companies with fewer than 1000 employees

The voluntary reporting framework for companies that are no longer directly within the scope of the CSRD is not yet precisely known.

However, the Commission indicates that this voluntary framework will be based on the VSME standards published in December 2024 by the EFRAG.

Today, double materiality analysis is not mandatory for companies that want to apply the VSME. However, this will be one of the major challenges of the negotiations that will take place in the coming weeks and months around the future voluntary framework. Many European deputies hope that double materiality will indeed be incorporated into this reporting framework, notably for the sake of coherence, as companies with more than 1,000 employees will apply double materiality and will ask for information from companies with fewer than 1,000 employees, which may only apply simple materiality.

3. Why perform your double materiality analysis?

Double materiality offers many advantages. By combining financial and impact dimensions, it allows companies:

- To assess their overall impact, understand all risks and opportunities, and be more transparent about their performance.

- To meet the growing expectations of stakeholders: investors, consumers, employees, etc. Conducting a double materiality analysis can strengthen their trust in the organization, offer a competitive advantage, confer a good reputation for the company, etc.

- To effectively prioritize issues and develop a roadmap of priorities. Double materiality allows them to know the changes to be implemented to ensure their sustainability, integrate environmental and social issues into their strategy and actions, notably through the implementation of responsible policies and practices.

4. How to perform your double materiality analysis?

{{newsletter-blog-2}}

It is important to note first that European standards do not impose the way in which double materiality should be conducted by companies, as a single process would not be suitable given the multiple sectors of activity, organizations, or value chains of the organizations concerned by the CSRD.

However, all CSRD stakeholders, starting with the EFRAG, agree on the same major steps, starting with the identification of the company's context (activities, stakeholders, etc.) up to the selection of material issues and the preparation of the reporting accordingly.

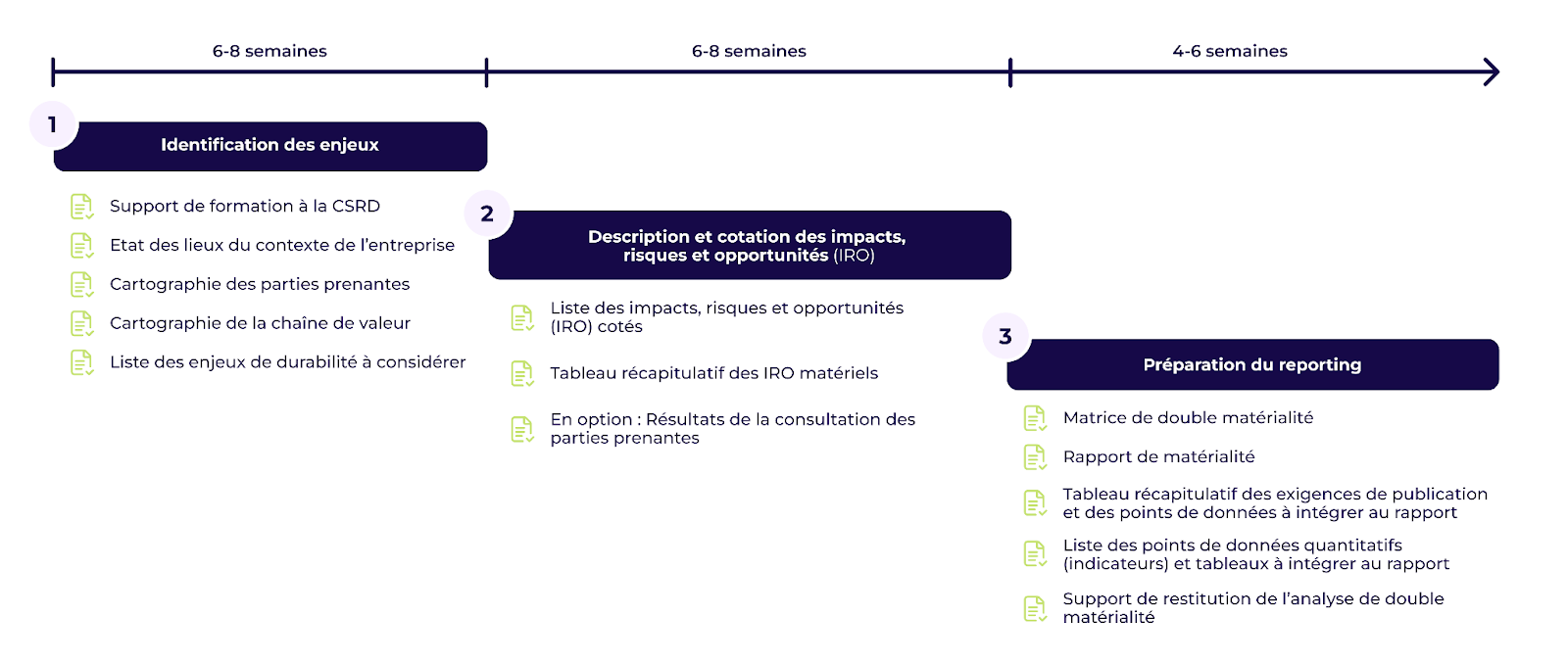

Thus, we can separate the approach into 3 major unavoidable steps.

4.1 Identification of issues for your double materiality

To do this, you need:

- A snapshot of the company's context

This involves understanding the company's activities, the products or services it sells, the locations where it operates, its financial statements, etc.

- A mapping of the value chain and stakeholders

The challenge is to trace the flows, map your value chain, both upstream and downstream, and then identify the stakeholders affected by the company's operations and throughout its value chain.

- Draw up a first list of sustainability issues to consider

This involves drawing up a list of all the issues that will then be analyzed from the perspective of double materiality in order to determine which ones are material.

To draw up this list, we do not start from scratch.

The first source is the list of sustainability issues provided by the EFRAG itself and which can be found in the ESRS 1, AR 16 (page 26 of this document). EFRAG details the themes, sub-themes, and sub-sub-themes that should be considered.

But this should not be the only source. This list should be supplemented by a documentary review to identify issues specific to the company through internal documents or a study of its sector of activity. Thus, a benchmark of the issues selected by the company's competitors can be very useful, as can the analysis of sector-specific voluntary frameworks published by the Sustainability Accounting Standards Board (SASB), the Global Reporting Initiative (GRI), or the Morgan Stanley Capital International (MSCI).

4.2 Description and scoring of impacts, risks, and opportunities (IRO) in the double materiality analysis

We are now entering the heart of double materiality, as it involves determining, based on the previously constructed list, which issues are material.

To do this, the organization must determine the impacts, risks and opportunities (IRO) related to sustainability issues across its value chain. Then it must apply evaluation criteria on impact materiality and financial materiality to determine which IROs are material.

Here are the criteria to consider:

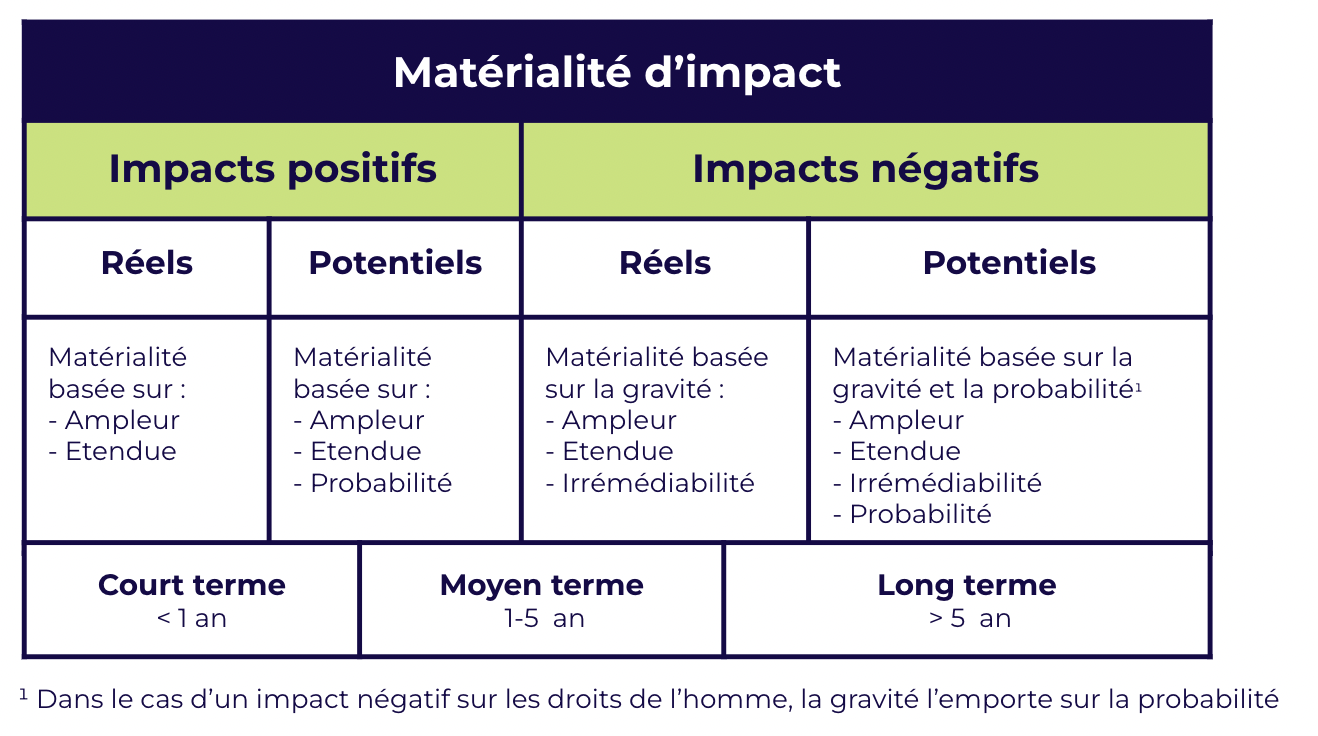

- For impact materiality

For negative impacts, it is the severity of the impact that is judged as well as its probability of occurrence for potential impacts. The criterion of impact severity itself depends on 3 criteria:

- its magnitude: how important or severe is the impact? On human rights or the environment for example.

- its extent: what is the scope of the impact? For example the extent of environmental damage

- and its irreparable nature: to what extent can the impact be repaired? Can environmental damage be restored and to what extent can the environment return to a situation at least equivalent to that observed before the negative impact?

For positive impacts, only the magnitude and extent of the impact are evaluated, as well as its probability of occurrence for potential impacts.

In summary:

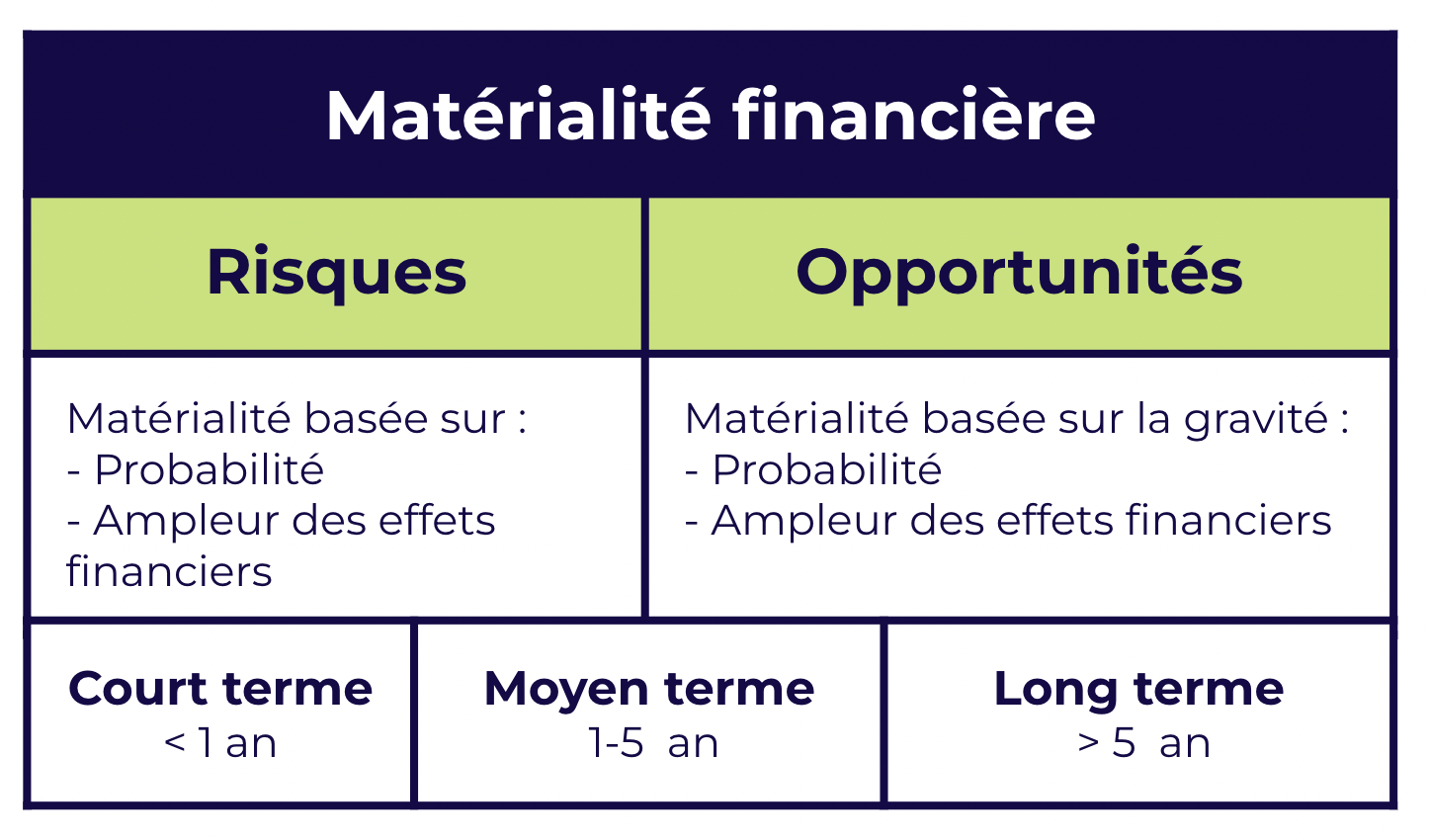

- For financial materiality

For reminder, financial materiality corresponds to the risks and opportunities generated by the economic, social and natural environment on the financial performance of the company.

To assess this financial materiality, two criteria must be considered:

- the potential magnitude of financial effects based on appropriate thresholds

- the probability of occurrence

This analysis must be done in the short, medium and long term.

Thresholds must therefore be used to determine the materiality or non-materiality of risks and opportunities. These can be absolute or relative monetary thresholds such as a percentage of the amount corresponding to its revenues, its costs, its total assets or its net worth.

A qualitative assessment must also be carried out since certain companies, due to their activities, are exposed to reputation risks. This risk, although it cannot be assessed, can influence the availability of financing and/or the cost of financing and, consequently, can be financially material.

For both materialities, impact and financial, the organization must then establish a customized scoring system to measure the intensity of each criterion: a scale from 0 to 3 for example, or from 1 to 5. It is up to the company to decide, the EFRAG does not impose a single methodology. Once the scoring system is established, it is finally necessary to define the thresholds beyond which the IROs will be considered as material.

Again, the EFRAG does not impose a methodology for choosing the threshold, qualitative or quantitative, for the company but the latter will have to justify how these thresholds were defined and applied.

Discover our article dedicated to the identification and evaluation of IRO

4.3 Preparing the double materiality reporting

This involves formatting the results and preparing the reporting accordingly.

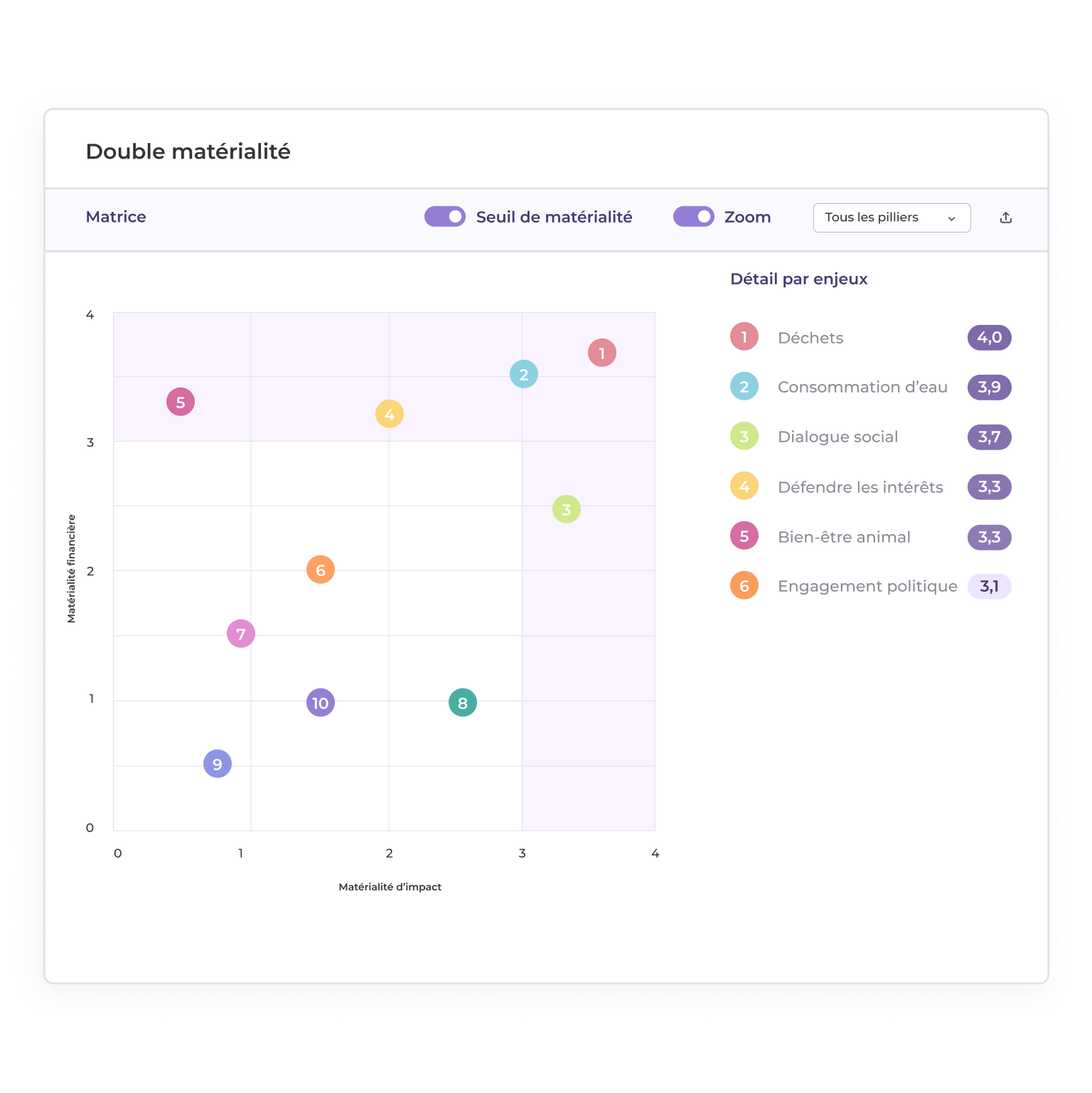

The preferred format remains the double materiality matrix which allows to simply visualize and prioritize material issues.

The company can then define what the publication requirements and the data points to be included in the sustainability report are.

5. How Sami helps you with the double materiality analysis?

Thanks to our CSRD module integrated into our platform and thanks to the support of specialized and selected consulting firms partners for their expertise, we are able to assist you with the realization of your sustainability report and in particular with your double materiality. Here is a summary of what we offer at each step.

5.1 On the identification of issues

Our consultants bring all their expertise to help the company draw up a first list of potentially material issues: construction of a benchmark of competitors, documentary review of international references, sector analysis, understanding of the organization's global context.

Our software allows you to map all your stakeholders in this first step (employees, customers, suppliers...) and adapt the ESRS framework to your situation. The list of sustainability issues, detailed by themes, sub-themes and sub-sub-themes, provided by EFRAG is integrated into our platform. You just have to parameterize the tool to adapt it to your issues.

5.2 On the description and scoring of impacts, risks and opportunities (IRO)

During this phase, our software allows, among other things:

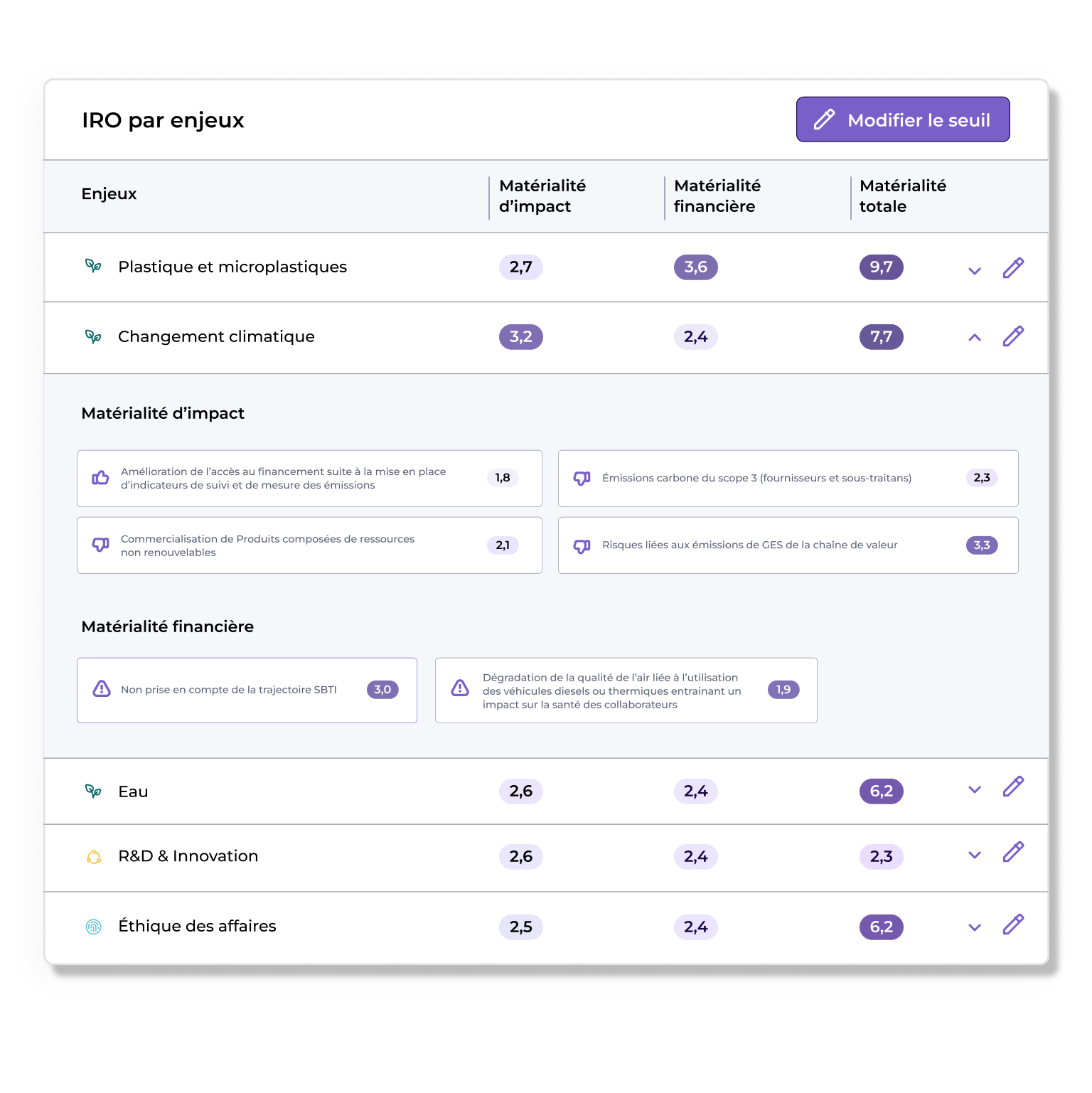

- Easily assess your IRO

For each of the defined material issues, the software provides a list of IRO. You determine the scoring of these IRO based on the criteria expected by EFRAG and the software automatically calculates the materiality score of each IRO. The evaluation grid is based on EFRAG standards.

The exercise begins with an on-site meeting with our consultants and the people in charge of the company's CSRD project to give you the keys to the scoring of the different IRO.

Our consultants follow this step with you, examine the results of the scoring for the first time (before any corrections if necessary) and prepare the summary table of material IRO, a deliverable required by ESRS 2.

- Engage your stakeholders

Reporting standards do not require setting up a dialogue with stakeholders for double materiality analysis.

However, exchanging with your stakeholders (internal and external) should first help you understand how they are or may be impacted and thus help you assess the severity and probability of impacts. It is therefore an important player in the construction of the materiality of your issues. And the dialogue with your stakeholders can also take place at a later stage, once the materiality is defined, in order to confirm or refute with them the materiality assessment.

That's why our software allows you to simply and effectively question the stakeholders you have identified. Ready-to-use questionnaire models and designed for CSRD are integrated. But you can also define your custom questionnaires with a multitude of available fields. Finally, the software automatically aggregates and analyzes the responses from your stakeholders to enrich the scoring of your IRO.

5.3 On the preparation of the report

Based on the scoring of IROs and the automatic calculation of materiality scores for each issue, our software automatically provides a double materiality matrix to allow you to visualize your material issues at a glance.

Our consultants also prepare the materiality report to detail the methodology followed and the results obtained (deliverable required in ESRS 2) and prepare a summary table of material issues, publication requirements and data points that will be integrated into the report.

In parallel, the software is configured to set up the data collection protocol and the drafting of the sustainability report.

{{newsletter-blog-3}}

Do you still have questions about double materiality analysis? You can consult our Q&A article on CSRD.

6. An example of double materiality analysis: the EBRA group

In this article, you will find the testimony of Rémy Ramstein, industrial, purchasing and CSR director of the EBRA press group (which owns 9 regional press titles in eastern France and employs 3,500 employees). He explains the process of preparing the group's first CSRD sustainability report and, in particular, their double materiality analysis.

Key points of the interview on their double materiality:

- Internal organization: The project is managed by a team (1.3 FTE) dedicated to CSR, with quarterly follow-up at the COMEX. Significant educational work was necessary to familiarize the management with the concepts of the CSRD.

- Stakeholder consultation: A total of 400 stakeholders were consulted, including 50 in individual interviews (COMEX members, internal and external experts) and 350 through questionnaires (employees, advertisers, readers).

- Analysis results: Out of 58 IROs initially identified, 38 were found to be material. These IROs have been grouped into sustainability issues for better readability in the double materiality matrix.

- Data collection: Approximately 400 data points need to be collected (compared to 300 for the previous DPEF), some of which were specifically created to represent the group's journalistic activity.

- Lessons: Rémy Ramstein emphasizes the importance of anticipating (at least one year of preparation), seeking expert support, and considering the CSRD not as a one-time project but as a continuous improvement process that enriches the company's CSR strategy.

Rémy Ramstein's testimony illustrates how compliance with the CSRD and, in particular, double materiality, beyond their regulatory aspects, have enabled the EBRA group to structure its CSR approach and establish a constructive dialogue with all actors in their value chain.

7. FAQ on double materiality analysis

What is double materiality in the context of the CSRD?

Double materiality is a central concept of the CSRD directive that combines two complementary perspectives: financial materiality (how the economic, social, and natural environment affects the company's financial performance - "Outside-In" vision) and impact materiality (how the company impacts its economic, social, and natural environment - "Inside-In" vision). This approach allows for a comprehensive assessment of a company's sustainable performance.

What is the difference between simple materiality and double materiality?

Simple materiality (or financial materiality) only considers the impacts of the environment on the organization's financial performance. This is the approach preferred by the ISSB. Double materiality, advocated by the EFRAG, adds a second dimension: the impact of the company on society and the environment. This more comprehensive approach allows for the identification of issues that might be overlooked in simple materiality.

How to structure a double materiality analysis?

It is structured in three main steps:

- Identification of issues: mapping of the company's context, value chain, and stakeholders, followed by the establishment of a preliminary list of sustainability issues.

- Description and scoring of impacts, risks, and opportunities (IRO): evaluation of IROs according to specific criteria for impact materiality and financial materiality.

- Preparation of reporting: formalization of the results and definition of publication requirements for the sustainability report.

How to define materiality thresholds for my company?

The EFRAG does not impose a single methodology for defining materiality thresholds. Each company must establish its own scoring system (for example, a scale from 0 to 3 or from 1 to 5) and define the thresholds beyond which IROs will be considered material. The company will need to justify how these thresholds were defined and applied in its sustainability report.

Is it necessary to consult stakeholders for the double materiality analysis?

Although the ESRS do not formally require stakeholder consultation, consulting them helps better understand how they are or may be impacted and thus more accurately assess the severity and probability of impacts. It is therefore a strongly recommended practice.

How much time should be planned to conduct a double materiality analysis?

According to the experience shared by companies that have already carried out this exercise, it is recommended to plan between 3 and 6 months. This timeframe allows for effective consultation of stakeholders, study of the results, and formalization of the conclusions.

How does the double materiality analysis fit with the other requirements of the CSRD?

Double materiality forms the basis of CSRD reporting. It helps determine which issues are material and therefore which publication requirements (data points) should be included in the sustainability report. Without this prior analysis, it is impossible to effectively structure your CSRD reporting.

Should the double materiality analysis be updated regularly?

Yes, it should be reviewed regularly to reflect the evolution of the economic, social, and environmental context in which the company operates. The ESRS recommend a review at least every 3 years or more frequently in case of significant changes.

How to use the analysis results beyond CSRD reporting?

The results can be used for:

- Enhance the company's CSR strategy

- Prioritize actions and investments in sustainability

- Structure dialogue with internal and external stakeholders

- Identify new business opportunities

- Anticipate emerging risks related to environmental, social, and governance issues

What are our other contents on CSRD?

- All the datapoints expected in this DR n°1 of the ESRS E1 (and all other datapoints) in this document: Sami: CSRD - ESRS Data Points.

- CSRD: understanding the ESRS E1 standard on climate change

- Building a transition plan aligned with CSRD

- The ESRS standards: Understanding European reporting criteria

Mission Décarbonation

Don't miss the latest climate news and stay ahead of regulatory changes

Discover our guide to successfully conducting a double materiality analysis

You will find the methodology, step by step, as well as the analysis of a CSR consultant

His double materiality analysis with Sami

Our specialized consultants support you in carrying out your double materiality assessment and a gap analysis.

Les commentaires